Configuration

The configuration files that affect CVA calculations are:

| Configuration File | Details |

| TaskList | A task of type CreditExposure must be set up in the task list. |

| Assumptions | Base assumptions common to all calculations. |

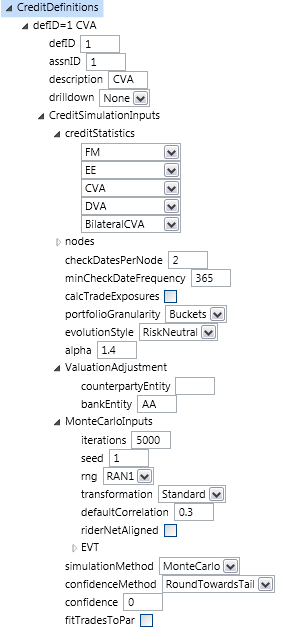

| CreditDefinitions | The fixed calculation timesteps (or nodes), choice of credit statistics (CVA, DVA, BilateralCVA), evolution style (should be set to risk neutral) and monte carlo inputs. |

| CreditCalculations | A calculation specifies a task name, counterparty/pool pair and CreditDefinition. Results are generated for each calculation specified. The counterparty and pool can use wildcards to allow many simulations to be specified by a single calculation. |

CVA Definition

Viewing Results of a CVA Calculation

Opening a successful CVA task from the summary page, a user can select a particular calculation to view its results. Here is a sample result:

The dropdown menu top right allows the user to select the following drilldown views:

- Exposure Profile (shown above)

- Portfolio Mtm on selected timestep

- Rate shifts on selected path

- Trade mtm and rates on selected timestep and path

- Rate shift on selected timestep and path

This large body of drilldown information is held in the risk engine’s results database. Typically, most of this information will not be generated in the production run. The policy is usually to wait until there is an issue before switching drilldown on and re-running the calculation.

Also appearing in the results viewer is a treeview containing all of the data required to re-run the calculation. This is where a user can prepare a re-run of the calculation with extra drilldown switched on.